We use cookies to improve your experience on our website. By continuing you acknowledge cookies are being used.

When is it time to access your super?

Super is your savings for retirement. So it makes sense that there is an age you have to reach to get access to the funds you’ve saved.

When you reach what we call your preservation age, you can access your super if you permanently retire. From 1 July 2024 this is age 60 for everyone.

So you’re old enough, now what?

Once you’ve celebrated your 60th birthday, there’s another box to tick before you get access to your super. We call this a condition of release and leaving the workforce for good is one of these conditions. So if you retire for good after reaching your preservation age, you can get your hands on your super.

If you change jobs on or after turning 60, you can continue to work and also access your super. Or you can wait until you reach age 65 and access your super, even if you’re still working.

If you become totally and permanently disabled before your preservation age, you’ll also be able to access your super.

Can you access your super before age 60?

Yes. But the Federal Government has very strict guidelines on when and why you can access you super early.

There are some other circumstances where you can apply to the Australian Tax Office to access a limited amount under compassionate grounds from your super before retirement, when you are in need of financial help, to:

Stop you from losing a home you own because you can’t pay the mortgage.

Cover the cost of medical treatment, palliative care and/or disability services for you or a dependent.

Cover the cost of a funeral or burial arrangements for a dependent.

You can also apply to your super fund for early access if you:

Are experiencing severe financial hardship, can’t pay basic expenses for you and your family and have been paid income support benefits like JobSeeker continuously for at least 26 weeks.

Have a terminal illness.

Become incapacitated, either, temporarily or permanently.

Is it a problem to access super early?

Any amount you take from super now is less money for when you retire. Of course, if being short of money is forcing hardship and stress on you now, and you have a legitimate reason to access your super, withdrawing an amount to take the pressure off makes sense. But it’s a good idea to get information on your other options before taking this step.

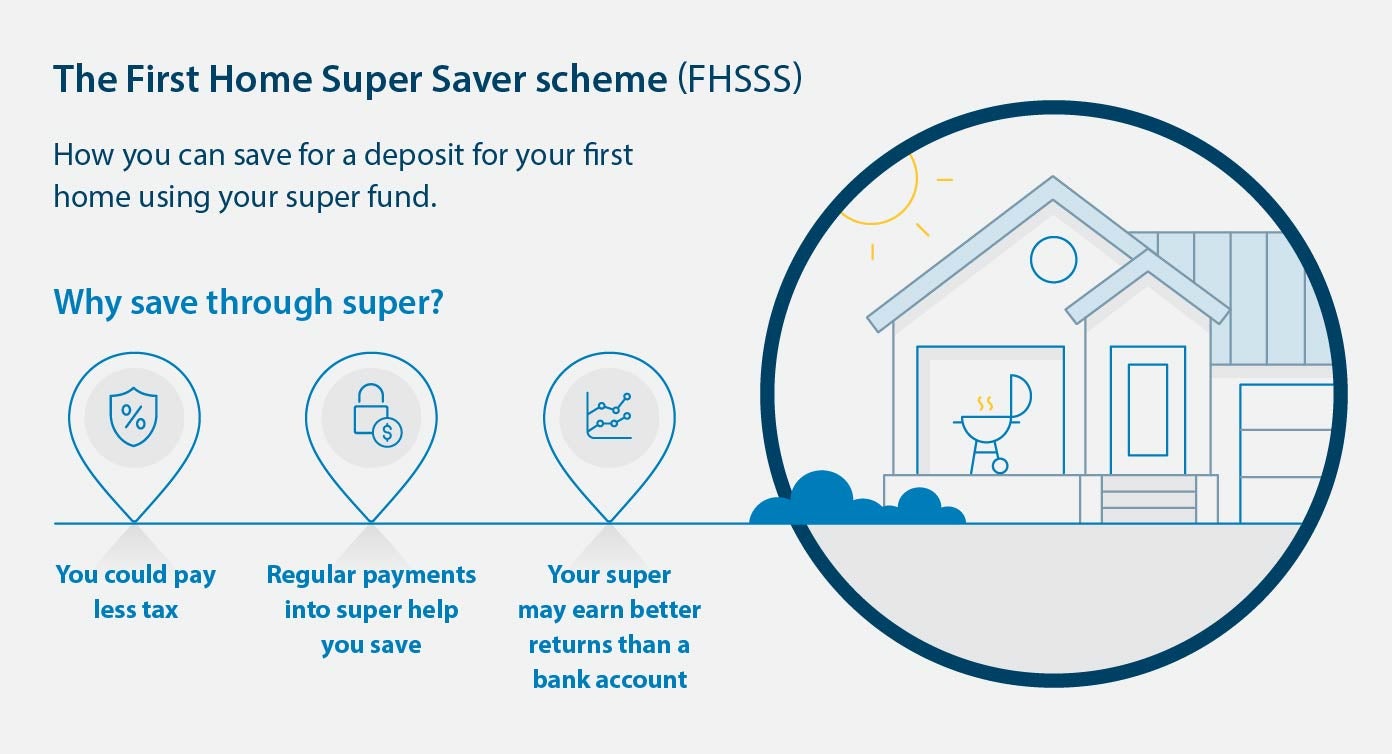

Can I really access my super to pay my first home deposit?

Yes you can. The First Home Super Saver Scheme (FHSSS) could see you on your way to owning your first home sooner:

You can only access any extra payments you have made into super for the purpose of saving for a home loan – and also investment returns those extra savings have created.

You can keep these payments in super until you’re ready to buy.

While you do this you can be saving on tax – both on the money you’re earning from investing your super savings, which is taxed within super at 15%, and from the tax you could save by making extra payments into super from your pre-tax salary – these are called concessional or salary sacrificed contributions.

- Regular payments into super help you save

- Your super may earn better returns than a bank account

Find out more about making extra super payments

Get the lowdown on the FHSSS and find out how you can save faster for your first step on the property ladder.